Blamed for Steam games ban, Mastercard encourages censorship during Riot Games VCT livestreams

Technology

132

Beiträge

79

Kommentatoren

14

Aufrufe

-

I have seen it mentioned quite a few times on websites. Can you actually pay normal shops using that?

I'm afraid it's not expanded to many countries just yet

-

FedNow became a thing just two years ago. With transaction fees of just $0.043/transaction, it's cheaper than every other payment processor out there. Hopefully it can gain adoption and push out Visa/Mastercard.

What prevents them from getting bigger and doing the same thing. This cycle of sadomasochism needs to stop at the root cause.

-

Credit cards should be illegal they are tools of Molloch and everyone loses at least a little from their usage.

Credit card payment charges should be itemized on the bill of any purchase and also rewards should be considered taxable income over 1000$/yearthey are tools of Molloch

dafuq

Credit card payment charges should be itemized on the bill of any purchase and also rewards should be considered taxable income over 1000$/year

I feel like we came to the same conclusions for very different reasons....

-

I'm in Europe and following the news of the MasterCard and Visa censorship I activelly went looking for how else could I pay for things online without using their networks, and as it turns out there are plenty of solutions supported by both Steam and GOG which I was just ignoring before because they just looked as lots of "weirdly named" unrecognized payment options.

I'm now using those in my purchases and so far they actually look more convenient than the Visa/MasterCard (for example, with iDEA which is Dutch, I can literally pay from my mobile phone banking app by just taking a picture of a QR-Code on my screen). The problem in Europe is just there being lots of local solutions and no EU-wide one yet, though I'm lucky because I have bank accounts in different countries (having lived in several countries in Europe) so I have access to many options.

Keep in mind that outside Britain, the rest of Europe have long had their own debit card withdrawal and payment networks and not relied on Visa/MasterCard (to me Britain was, frankly, weird in that it relies on mainly VISA Debit and had no local payment solution, probably explained by lack of political will in the UK for that: most such payment networks in Europe were born out of political pressure on banks to come up with a standard and sometimes were even started as state-owned companies) so a lot of these local online payment options are extensions of those existing networks, which is probably why trying come up with an single integrated cross-border payment processor has been slow going.

That said, thanks to it having been mandated at the EU level, bank transfers are nowadays fully cross-border integrated and you can transfer money between accounts anywhere in EU with the same ease and for the same cost you can for local accounts (the banks really resisted that, by the way, as it took away most of their "international transfers" profits) so we're probably not far from a single EU-wide payment processor (or at least EU-wide account support on existing solutions).

-

Why do payment processors have the ability to control morality in our world? Easily the definition of a monopoly. Absolutely insane.

Because we, collectively as a society, gave them that power.

Clearly, that was a mistake.

-

did anyone mentioned that all these bans were all pushed by russel vought.

Fits the definition of the wealthy "moving their will throughout the world"

-

Credit cards should be illegal they are tools of Molloch and everyone loses at least a little from their usage.

Credit card payment charges should be itemized on the bill of any purchase and also rewards should be considered taxable income over 1000$/yearCredit cards should be treated as utilities. They shouldn't be able to restrict my legal purchases.

-

What prevents them from getting bigger and doing the same thing. This cycle of sadomasochism needs to stop at the root cause.

FedNow is ran by the Federal Reserve. They are almost certainly going to retain stricter regulation than independently operated payment processors.

-

I'm in Europe and following the news of the MasterCard and Visa censorship I activelly went looking for how else could I pay for things online without using their networks, and as it turns out there are plenty of solutions supported by both Steam and GOG which I was just ignoring before because they just looked as lots of "weirdly named" unrecognized payment options.

I'm now using those in my purchases and so far they actually look more convenient than the Visa/MasterCard (for example, with iDEA which is Dutch, I can literally pay from my mobile phone banking app by just taking a picture of a QR-Code on my screen). The problem in Europe is just there being lots of local solutions and no EU-wide one yet, though I'm lucky because I have bank accounts in different countries (having lived in several countries in Europe) so I have access to many options.

Keep in mind that outside Britain, the rest of Europe have long had their own debit card withdrawal and payment networks and not relied on Visa/MasterCard (to me Britain was, frankly, weird in that it relies on mainly VISA Debit and had no local payment solution, probably explained by lack of political will in the UK for that: most such payment networks in Europe were born out of political pressure on banks to come up with a standard and sometimes were even started as state-owned companies) so a lot of these local online payment options are extensions of those existing networks, which is probably why trying come up with an single integrated cross-border payment processor has been slow going.

That said, thanks to it having been mandated at the EU level, bank transfers are nowadays fully cross-border integrated and you can transfer money between accounts anywhere in EU with the same ease and for the same cost you can for local accounts (the banks really resisted that, by the way, as it took away most of their "international transfers" profits) so we're probably not far from a single EU-wide payment processor (or at least EU-wide account support on existing solutions).

The banking sector is very competitive in the UK compared to pretty much any other country, so dodgy behaviour from banks/payment processors wasn't very frequent.

More recently, however, just like the EU, the UK is working on their own system right now. The EU doesn't have a unified payment processing system either, just a patchwork of different ones.

-

I'm in Europe and following the news of the MasterCard and Visa censorship I activelly went looking for how else could I pay for things online without using their networks, and as it turns out there are plenty of solutions supported by both Steam and GOG which I was just ignoring before because they just looked as lots of "weirdly named" unrecognized payment options.

I'm now using those in my purchases and so far they actually look more convenient than the Visa/MasterCard (for example, with iDEA which is Dutch, I can literally pay from my mobile phone banking app by just taking a picture of a QR-Code on my screen). The problem in Europe is just there being lots of local solutions and no EU-wide one yet, though I'm lucky because I have bank accounts in different countries (having lived in several countries in Europe) so I have access to many options.

Keep in mind that outside Britain, the rest of Europe have long had their own debit card withdrawal and payment networks and not relied on Visa/MasterCard (to me Britain was, frankly, weird in that it relies on mainly VISA Debit and had no local payment solution, probably explained by lack of political will in the UK for that: most such payment networks in Europe were born out of political pressure on banks to come up with a standard and sometimes were even started as state-owned companies) so a lot of these local online payment options are extensions of those existing networks, which is probably why trying come up with an single integrated cross-border payment processor has been slow going.

That said, thanks to it having been mandated at the EU level, bank transfers are nowadays fully cross-border integrated and you can transfer money between accounts anywhere in EU with the same ease and for the same cost you can for local accounts (the banks really resisted that, by the way, as it took away most of their "international transfers" profits) so we're probably not far from a single EU-wide payment processor (or at least EU-wide account support on existing solutions).

Cries in American

-

The banking sector is very competitive in the UK compared to pretty much any other country, so dodgy behaviour from banks/payment processors wasn't very frequent.

More recently, however, just like the EU, the UK is working on their own system right now. The EU doesn't have a unified payment processing system either, just a patchwork of different ones.

I lived in the UK and worked in the Finance Industry there, as well as in a couple of other countries in Europe, and the idea that the UK banking sector is "very competitive [...] compared to pretty much any other country" or there not being frequent dodgy behaviours from banks/payment processors is hilariously.

Just look at how a physical payment with one's debit card (which goes directly to the bank account) can trigger oversized "uncovered overdraft fees" rather than just deny the payment if there are not enough funds in the account for that card like in countries like Portugal and The Netherlands: I literally dumped the first bank I had in the UK when I moved there from The Netherlands exactly because they charged me £30 overdraft fees on a payment ON A DEBIT CARD because my current account which was directly linked to it had £5 less than the amount I was trying to pay (plenty of money on the savings account though), rather than the payment attempt being rejected, even though when I first got that account I explicitly enquired about it I was told payments attempts on that card without enough funds would be rejected.

UK banking is riddled with insane fees for every little possible thing imaginable (especially user mistakes), from presential payments where the account doesn't have enough funds (where instead of the payment being denied they charge you money) to things like getting a paper bank statement from the bank and those fees are invariably many times more than the actual cost for the bank of it - "competition" between banks in the UK is purelly slimy "introductory rates" that change after a year or two for highly visibly stuff whilst everything that's standard with the account anywhere else costs extra in the UK and every customer mistake results in a punitive charge.

Even in my homeland of Portugal, where banking is pretty much a cartel where all the big institutions regularly buy politicians from both main parties with non-executive board memberships and gold-plated consulting gigs (in all fairness, in the UK it's the same), banking is nowhere as slimy and abusive as in Britain.

I get the impression you never had a bank account anywhere else if you think banking in the UK is "very competitive" and that the frequency of "dodgy behaviours" is low there, because comparativelly with where I lived and banked elsewhere in Europe, retail banking in the UK is a totally disgraceful leech-filled swamp.

Or maybe it's me having "lived a blessed life" in terms of my banking because I've only ever lived and banked in Europe.

As for the rest, Europe doesn't have a unified payment processing system but pretty much each country in it has one, whilst in the UK there is no such thing at all and instead mainly Visa is used. As for they're "working on it", in my personal experience in Britain it means nothing at all because all the cunts in leadership positions in both Government and Finance over there are liars who regularly get away with it: going with "it ain't happenning until it actually happens" when it comes to the promises of those people is the most successful posture over there if you're not an insider by far.

-

I lived in the UK and worked in the Finance Industry there, as well as in a couple of other countries in Europe, and the idea that the UK banking sector is "very competitive [...] compared to pretty much any other country" or there not being frequent dodgy behaviours from banks/payment processors is hilariously.

Just look at how a physical payment with one's debit card (which goes directly to the bank account) can trigger oversized "uncovered overdraft fees" rather than just deny the payment if there are not enough funds in the account for that card like in countries like Portugal and The Netherlands: I literally dumped the first bank I had in the UK when I moved there from The Netherlands exactly because they charged me £30 overdraft fees on a payment ON A DEBIT CARD because my current account which was directly linked to it had £5 less than the amount I was trying to pay (plenty of money on the savings account though), rather than the payment attempt being rejected, even though when I first got that account I explicitly enquired about it I was told payments attempts on that card without enough funds would be rejected.

UK banking is riddled with insane fees for every little possible thing imaginable (especially user mistakes), from presential payments where the account doesn't have enough funds (where instead of the payment being denied they charge you money) to things like getting a paper bank statement from the bank and those fees are invariably many times more than the actual cost for the bank of it - "competition" between banks in the UK is purelly slimy "introductory rates" that change after a year or two for highly visibly stuff whilst everything that's standard with the account anywhere else costs extra in the UK and every customer mistake results in a punitive charge.

Even in my homeland of Portugal, where banking is pretty much a cartel where all the big institutions regularly buy politicians from both main parties with non-executive board memberships and gold-plated consulting gigs (in all fairness, in the UK it's the same), banking is nowhere as slimy and abusive as in Britain.

I get the impression you never had a bank account anywhere else if you think banking in the UK is "very competitive" and that the frequency of "dodgy behaviours" is low there, because comparativelly with where I lived and banked elsewhere in Europe, retail banking in the UK is a totally disgraceful leech-filled swamp.

Or maybe it's me having "lived a blessed life" in terms of my banking because I've only ever lived and banked in Europe.

As for the rest, Europe doesn't have a unified payment processing system but pretty much each country in it has one, whilst in the UK there is no such thing at all and instead mainly Visa is used. As for they're "working on it", in my personal experience in Britain it means nothing at all because all the cunts in leadership positions in both Government and Finance over there are liars who regularly get away with it: going with "it ain't happenning until it actually happens" when it comes to the promises of those people is the most successful posture over there if you're not an insider by far.

So much text here, and yet so incorrect. Little fees? Lol, so uninformed. The amount of little fees for things you get charged for by banks pretty much anywhere outside of the UK is pretty crazy.

Then topped off with a "they're working on it? Well I say they're not!!!" lmao

At least try to make your post believable if you're going to lie.

-

So much text here, and yet so incorrect. Little fees? Lol, so uninformed. The amount of little fees for things you get charged for by banks pretty much anywhere outside of the UK is pretty crazy.

Then topped off with a "they're working on it? Well I say they're not!!!" lmao

At least try to make your post believable if you're going to lie.

So you don't actually have any personal experience of banking anywhere else than Britain and your "even bankings is great in Great Britain" statements are nothing more than nationalistic bollocks.

Cheers for confirming my earlier impression.

-

FedNow is ran by the Federal Reserve. They are almost certainly going to retain stricter regulation than independently operated payment processors.

I’m. So. Reassured.

-

So you don't actually have any personal experience of banking anywhere else than Britain and your "even bankings is great in Great Britain" statements are nothing more than nationalistic bollocks.

Cheers for confirming my earlier impression.

I've banked in South Africa, the Netherlands, Germany, Australia, New Zealand, Poland, Ireland, and the UK. More if you include using British or Polish bank accounts in other countries. The banking sector in the UK is by far and away the most competitive of all those places. Fees are basically non-existent.

You think it's nationalist to say the UK has a competitive banking sector? Lmao you are crazy. I think you're projecting there.

I caught you blatantly lying. £30 fee for being overdrawn? That's way above the legal limit. It literally couldn't have happened. The most you will have been charged for being £5 overdrawn is the amount overdrawn with a 40% APR, for the amount of days overdrawn.

I.e. if you were overdrawn by £5, then didn't move £5 back into your account by the end of the day, you would've been charged (5*1.4)/365=£0.02

I tell you that in fact, just like the EU, a new payment processing system is being created, and you go straight into denialism and pretend it's not happening.

Take your weirdly-placed xenophobia out of here. I don't know why you're lying over something so inconsequential.

-

You can't control what we jack off to, Mastercard.

-

I'm in Europe and following the news of the MasterCard and Visa censorship I activelly went looking for how else could I pay for things online without using their networks, and as it turns out there are plenty of solutions supported by both Steam and GOG which I was just ignoring before because they just looked as lots of "weirdly named" unrecognized payment options.

I'm now using those in my purchases and so far they actually look more convenient than the Visa/MasterCard (for example, with iDEA which is Dutch, I can literally pay from my mobile phone banking app by just taking a picture of a QR-Code on my screen). The problem in Europe is just there being lots of local solutions and no EU-wide one yet, though I'm lucky because I have bank accounts in different countries (having lived in several countries in Europe) so I have access to many options.

Keep in mind that outside Britain, the rest of Europe have long had their own debit card withdrawal and payment networks and not relied on Visa/MasterCard (to me Britain was, frankly, weird in that it relies on mainly VISA Debit and had no local payment solution, probably explained by lack of political will in the UK for that: most such payment networks in Europe were born out of political pressure on banks to come up with a standard and sometimes were even started as state-owned companies) so a lot of these local online payment options are extensions of those existing networks, which is probably why trying come up with an single integrated cross-border payment processor has been slow going.

That said, thanks to it having been mandated at the EU level, bank transfers are nowadays fully cross-border integrated and you can transfer money between accounts anywhere in EU with the same ease and for the same cost you can for local accounts (the banks really resisted that, by the way, as it took away most of their "international transfers" profits) so we're probably not far from a single EU-wide payment processor (or at least EU-wide account support on existing solutions).

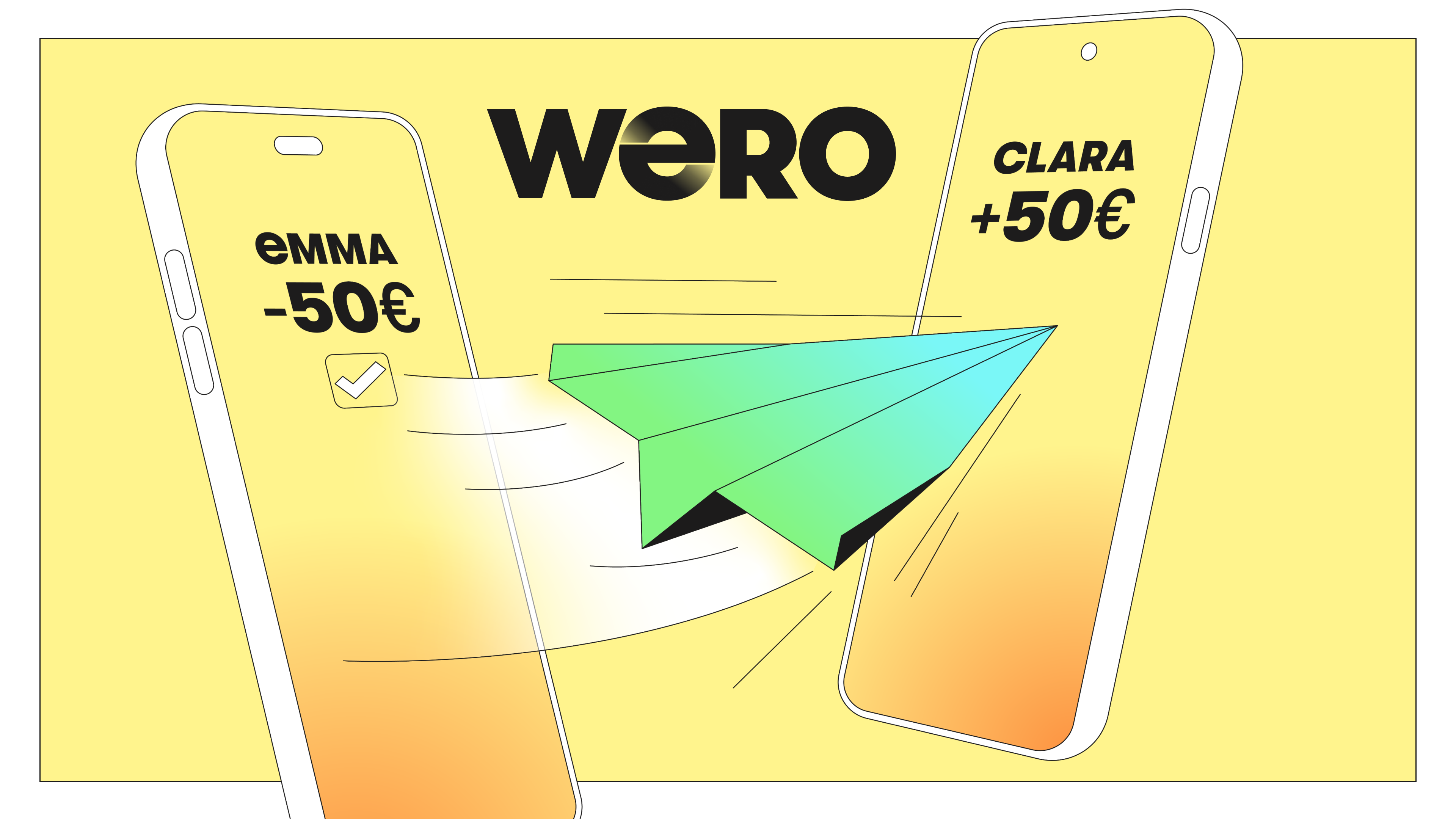

There is a EU-wide payment option.

Wero - Digital payment wallet

Experience fast and secure digital payments with Wero’s wallet, enabling you to send and receive money between bank accounts in under 10 seconds.

(wero-wallet.eu)

-

The banking sector is very competitive in the UK compared to pretty much any other country, so dodgy behaviour from banks/payment processors wasn't very frequent.

More recently, however, just like the EU, the UK is working on their own system right now. The EU doesn't have a unified payment processing system either, just a patchwork of different ones.

Wero - Digital payment wallet

Experience fast and secure digital payments with Wero’s wallet, enabling you to send and receive money between bank accounts in under 10 seconds.

(wero-wallet.eu)

-

What prevents them from getting bigger and doing the same thing. This cycle of sadomasochism needs to stop at the root cause.

Enshitification is common. Corps care a ton about social pressures and norms. They get swayed easily by public opinions.

This one is US Gov based so we'll see how it plays out. They tend to be slower to move... Until someone starts slinging executive orders around to rip things out and tear them down.

-

I've banked in South Africa, the Netherlands, Germany, Australia, New Zealand, Poland, Ireland, and the UK. More if you include using British or Polish bank accounts in other countries. The banking sector in the UK is by far and away the most competitive of all those places. Fees are basically non-existent.

You think it's nationalist to say the UK has a competitive banking sector? Lmao you are crazy. I think you're projecting there.

I caught you blatantly lying. £30 fee for being overdrawn? That's way above the legal limit. It literally couldn't have happened. The most you will have been charged for being £5 overdrawn is the amount overdrawn with a 40% APR, for the amount of days overdrawn.

I.e. if you were overdrawn by £5, then didn't move £5 back into your account by the end of the day, you would've been charged (5*1.4)/365=£0.02

I tell you that in fact, just like the EU, a new payment processing system is being created, and you go straight into denialism and pretend it's not happening.

Take your weirdly-placed xenophobia out of here. I don't know why you're lying over something so inconsequential.

Sure mate, banking in Britain is the Greatest In The World, you being a Briton rushing to claim Britain's banking sectors is the most competitive "compared to pretty much any other country" is not at all driven by "love of the Fatherland".

Oh, and by the way, check the law on overdraft fees a decade and a half ago before you call others liars.

En zeker, het is absoluut gelovelijk dat je in Nederlands en Zuid-Afrika gewoont en bankiered heben.